Lina Khan Finally Gets Her Merger Tax, Now What?

Abusing process to deter business is the Khan FTC's signature move. Now, it has new rules that tax all mergers. The Republicans stopped a larger tax by going along with it. Was that the right call?

Welcome back to Competition on the Merits. Today we take on a challenging task. Perhaps the most challenging to date. I’m going to try to get you to care about antitrust process and procedure. Specifically, the merger review process. Don’t leave yet. Specifically, we are going to talk about the Hart-Scott-Rodino (HSR) Act of 1976 and the process it lays out for merger review. The FTC issued radical, sweeping changes to the HSR process for the first time since 1978 – making changes to the initial HSR form firms file when they intend to merge. The new HSR rule was finalized Thursday by a 5-0 vote with the two Republican Commissioners joining the Democratic majority.

If it was a unanimous vote can it be so bad? Yeah, I think so. But this is a pretty mixed bag. The two Republican Commissioners faced a tough choice: (1) compromise and negotiate away the worst parts of the proposed HSR rule for something less terrible and less likely to be found unlawful; or (2) a 3-2 partisan dogfight over the proposed HSR rule with dissents that highlight its infirmities for the courts in an upcoming challenge. I would like to think I’ve earned my stripes in terms of thinking about when and where an FTC Commissioner should dissent and some of the strategic tradeoffs involved in those decisions. So I’ll end today’s newsletter talking about my own views of that calculus from here on the sidelines. But we have some work to do first.

So I can convince you to read on – here is where we are heading:

Merger process is a really big deal and is actually the most economically harmful part of the Biden-Harris Antitrust Regime

Khan-Kanter have been on a merger process offensive that really only makes sense if you hold the view that all mergers are bad

The Notice of Proposed Rulemaking (NPRM or Proposed Rule) was unlawful and a humongous tax on M&A Activity that will be borne disproportionately by smaller firms

The revised, Final Rule is rule is a lot better – the Republican Commissioners got a ton of really bad stuff out of it — two cheers for them

But the Final Rule is still a slightly less humongous tax on M&A activity – one that almost certainly does not survive a cost-benefit test – and it still might not be lawful

The Republican Commissioners get two out of a possible three cheers here. They bargained shrewdly to get the worst part of the NPRM discarded and even brought back Early Termination

But they gave up the opportunity to reject the Proposed Rule and dissent on the grounds that it is not consistent with cost-benefit analysis. I favor the latter strategy but theirs is more than defensible

A legal challenge is coming to the Final Rule – I preview the arguments

That is where we are headed. Let’s get to work. And of course, first thing – subscribe, tell a friend to subscribe, subscribe again – or upgrade to paid.

Why Should You Care About HSR and Merger Process?

Merger process is a really big deal. The FTC and DOJ receive thousands of HSR reportable transactions each year. 1,805 in FY 2023 to be exact. 3,152 in 2022. But for purposes of our discussion here the historical average is around 2,000 a year over the last decade. The required HSR form along with the merger filing fee (ranging from $30,000 to $2.335 million depending upon the size of the transaction) triggers the merger review process.

The merger review process is expensive! The FTC estimated it takes about 37 hours to complete the old HSR form at a cost of $17,200. That estimate uses an hourly rate of $460 — not a chance. A Chamber of Commerce survey of experienced antitrust practitioners estimated about 85 hours of work and a rough filing cost of $80,000. That was with the old HSR form. We will get into the revised form details in a second – and what extra burdens it introduces – but experts estimate the proposed revised form would take something like 327 hours of lawyer time and about 33 days to complete at a cost of about $300,000.

Before you say – “but those mega-corporations can handle the cost! $300,000 is nothing to Google or Amazon!” Remember two things: (1) both sides of a deal file HSR forms, the acquirer and the acquired firm, so each bears the cost; and (2) there are a thousands of HSR filings for smaller companies and smaller deals. And that $300,000 is just the time and money to complete the initial form to enter into a voluntary transaction between two firms!

The really significant costs are borne by merging parties after the HSR filing.

Khan-Kanter Are Not Especially Active or Effective Merger Law Enforcers, But They Are Especially Talented at Using Process to Kill Deals

This is a take that you are positive is wrong if you just read the glowing profiles from the NY Times, and Bloomberg, and Time, and then Bloomberg again. Or the glamorous and dramatic spread in Rolling Stone. If you read the headlines, Khan and Kanter are out busting monopolies and stopping mergers in court left and right. On top of that – the FTC and DOJ were simply asleep behind the wheel for the past 40 years. That is the story as they tell it. And the one the sympathetic journalists go along with.

But Competition on the Merits readers know that is not what the data show. What the data show are that Khan and Kanter’s merger enforcement agenda:

Loses more often in court than any in the modern era

Is no more active in court than their predecessors – so it is not as if the subpar win-loss record is explained by taking more risky cases

Does not score more merger consents than predecessors either

You don’t believe me. Fine. Here are the data. There are a couple of pending litigations so we can update them in a few weeks. But they tell the story just fine. And I’ve gone into detail discussing the Trump versus Biden merger enforcement records here.

Bottom line? Though the mainstream headlines are committed to a different narrative, the Trump antitrust agencies were as active (slightly more, even) as the Biden FTC and DOJ. The Trump agencies blocked 4.75 mergers per year compared to 4.71 merger blocks per year for the Biden administration. Compare that to the 3.25 mergers blocked per year during the Obama administration and 2.38 mergers blocked per year during the Bush years. If we broaden the analysis to include all forms of agency influence on a deal (blocked, abandoned, or settled) we get a slightly different picture: the Trump FTC/DOJ blocked, forced abandonment or settled 24.50 deals / year compared to 12.94 for the Biden merger enforcers. NY Times and Bloomberg just missed while in line for an autograph I guess. And don’t get me wrong, they are not especially bad either. It is the same talented staff bringing most of these cases with a little more managerial interference than before.

But if the Biden-Harris FTC and DOJ are nothing special when it comes to merger review – why are people so upset about Khan (especially) and Kanter? From Andreesen & Horowitz and the Little Tech Agenda, to Harris supporters like Mark Cuban and Reid Hoffman campaigning against a second term for Chair Khan, to Republicans pointing out the merger enforcement approach has been a general and broad tax against all M&A activity. How does all of the objection to Khan-Kanter merger enforcement make any sense when there is not that much of it in court? The answer: It’s the merger process.

The Khan FTC has been on a mission to make it harder to merge using HSR and other tools. Notice that I did not say the Khan FTC (and Kanter DOJ) have been using HSR and other process tools to target anticompetitive deals. That would be a feature, not a bug. But when one has expressed the worldview that all mergers and acquisitions are a social bad, it is not surprising that we see procedural, sub rosa attempts to kill deals whether or not they raise any competition concerns. You want examples? OK.

The FTC and DOJ abandoned early termination – a process the FTC and DOJ had used to give efficient and expedited approval to mergers that did not raise any competitive concerns.

The FTC withdrew its bipartisan 1995 Policy Statement that it would not seek prior approval in merger cases (i.e. force a party to agree that all future mergers would need to be approved by the FTC, thus giving up the party’s right to go to court, in order to have a merger approved). Commissioner Phillips wrote an excellent dissent on that one.

The FTC sent letters to companies, including ones it was not investigating, threatening to break up mergers.

Congress even went so far as to propose banning all mergers during the pandemic.

FTC and DOJ have used all of these procedural tools, and the HSR process, to make it harder and harder for parties to get deals through the regulatory process.

How much harder? The excellent Dechert DAMITT tracker shows that duration of significant investigations used to average about 8.1 months from 2011-2016. During the Biden-Harris years that average has jumped significantly, adding about 3 months time to the typical significant investigation.

The time and money associated with that delay is significant for merging parties – both the acquiring firm and the (often, smaller) acquired firm. Former Commissioner Phillips describes the impact of this Process M&A Tax nicely:

Exactly right – and well said. Of course, if your worldview is that all M&A activity is bad, a broad based tax in terms of time and significant expense on HSR process is a good thing. Of course, that worldview is wrong on the facts and the economics. But it does explain the full procedural assault on mergers that has been happening within the bowels of the FTC and DOJ over the past 4 years and why observers are put off by it. Recall again, most of these costs are imposed on deals with absolutely no competitive issues whatsoever. And as Phillips points out, the real problem here is for smaller firms who bear a much bigger burden and are more likely to fold and abandon transactions due to process pain than are Google or Amazon.

That full on assault on mergers through procedural shenanigans and delay is the main character in objections to Khan’s FTC. Now you know. And it is really important to understand that context in order to evaluate the action on the Final Rule. Let’s do a very quick HSR Primer – because it is impossible to understand why this stuff really matters without it.

A Very Quick HSR Primer

The HSR Act of 1976 was a watershed for merger enforcement. Prior to the HSR Act, most antitrust enforcement related to mergers was conducted after the transaction was consummated. Even when lawsuits were successful, it was often very difficult to “unscramble the eggs” when companies had already merged assets. The HSR Act modernized merger enforcement by creating a premerger system and allowing agencies a limited time prior to the transaction closing to analyze the proposed merger for competitive problems.

The basic idea of the Premerger Notification program is that agencies can challenge deals prior to consummation, making remedies much more effective. While it is generally agreed upon that the HSR Act has made process more efficient compared to challenging long consummated mergers, there is also widespread belief that the costs imposed during the process have become remarkably burdensome and have been heading that direction for decades.

After all, Congress intended the HSR Act not to impose broad costs on all mergers, but rather “the very largest corporate mergers – about the 150 largest out of the thousands that take place every year”? Well, with about 2000 HSR filings annually, we know that we are already far from what Congress intended. But the burden of the HSR process has really exploded over the years.

First, let’s talk about the process.

Filing: It begins with the parties submitting an HSR filing to notify the agencies of a proposed deal. After signing a deal parties must file their respective HSR forms with both the FTC and DOJ. As discussed, estimates of the time to complete the “old” HSR form run about 10 days and cost estimates run somewhere around $80,000. The HSR filing starts an initial 30 day waiting period where the agency can decide whether to issue a Second Request or allow the deal to clear.

Clearance. Once HSR forms are filed. The “Clearance” process begins. This is an opaque process involving a “liaison” agreement between the DOJ and FTC to prevent duplicative investigations. A few outcomes are possible here:

Neither FTC nor DOJ want to open a preliminary investigation and – at least in the old days – the deal might be granted early termination. Under the Biden-Harris administration, those deals – which pose no competitive risks – just sit and wait for the initial 30 day waiting period to expire before moving forward.

One agency but not both want to open a preliminary investigation and that agency does so.

Both agencies want to open the investigation. In this case there is a political back and forth to allocate the investigation. In theory it is informed by prior experience with the industry at issue and relevant expertise. In practice, clearance battles can run until the very last day of the initial 30 day waiting period – that is, merging parties may be told on day 30 of 30 that the FTC (or DOJ) has been granted clearance to open a preliminary investigation into the deal.

Just to give a sense of numbers here, for the past 24 years the number of preliminary investigations between both the FTC and DOJ averages around 250. In 2021 about 8% of HSR reportable transactions resulted in a preliminary investigation. In FY 2023 the number of clearances granted to the FTC or DOJ was 185. See Table III below.

Second Requests. We are going to focus here mostly on the HSR form itself — and less on the “back end” of the HSR process. But just to complete the loop for context. The HSR Act authorizes the investigating agency to issue a Request for Additional Information and Documentary Material (Second Request) if the agency determines that an in-depth investigation is warranted. The agencies have until the end of the 30 day initial waiting period to decide whether to issue a Second Request. The issuance of the Second Request triggers an obligation for the parties to “substantially comply,” which in turns starts a second (usually) 30 day clock for the agency to make a decision. So for transactions that reach the Second Request phase the process looks something like:

HSR filing triggers the initial 30 day waiting period;

Preliminary investigation cleared to either the FTC or the DOJ

Parties receive a Voluntary Access Letter (VAL) from the investigating agency

Parties engage with the agency on the merits and try to resolve concerns

Agency issues Second Request

Parties substantially comply with the Second Request, triggering the second 30 day waiting period

Continued advocacy and engagement with the investigating agency

Agency decides whether or not to seek a preliminary injunction enjoining the deal under the Clayton Act, reach a settlement with the parties resolving concerns, or close the investigation before the expiration of the second 30 day waiting period

A subject for another day, but sometimes the parties will voluntarily enter into “timing agreements” that give the agency extra time to reach a decision. Why? Mostly because it may beat being sued or because the extra time is useful in entering into consent negotiations.

Substantial compliance with a Second Request is incredibly expensive. The Second Request is a massive undertaking itself – reserved for transactions which the investigating agency believes might raise competitive concerns under the Clayton Act. It covers e-mails, electronic documents, data, information on the deal rationale, strategic and pricing documents, and more that the parties must collect from tens or even over 100 document custodians. The agency often takes depositions of multiple representatives from each party. At this stage parties are also usually submitting (expensive) economic expert analysis. The point is – this is a massive undertaking and can be very expensive. Some estimates put the cost of substantial compliance to the parties between $10 and $20 million dollars.

In FY 2023 you can see that for 1,735 HSR transactions there were only 185 preliminary investigations and, out of those, just 37 Second Requests – about 2.1% of HSR reportable transactions resulted in a Second Request.

Back to Preliminary Investigations. Recall that the preliminary investigation is really the first step after the HSR filing for those transactions that potentially raise competition issues. Historically, this has been about 10 percent of all HSR filings. That first step happens relatively quickly! FTC or DOJ staff may contact the merging parties within the first week or so of filing the HSR. The agency is “on the clock” with its initial 30 day waiting period from the date the HSR filing is submitted and must decide whether or not to issue a Second Request. Of course, the agency also has substantial leverage given the substantial cost of complying with the Second Request. So companies have significant incentives to cooperate with the agency during the preliminary investigation stage – and will often agree to give the agency more time to complete its investigation than the HSR Act allows to avoid those costs.

The primary vehicle the agency has for gathering information during the preliminary investigation is by issuing a voluntary access letter (VAL). The VAL is a fairly extensive “request” for more information. And again, voluntary only in the sense that the agency retains the ability to issue the Second Request and impose substantial compliance costs on any party that chooses not to voluntarily submit information. Here’s a description of the VAL and the sort of information requested from the FTC website:

The FTC used to publish a sample VAL on its website. It is gone now. You’ll see why in a second.

The punchline here is that under the Final Rule, the FTC now requires information historically requested through a VAL (and more) - previously reserved for the small percentage of mergers subject to preliminary investigations - to be submitted in the initial HSR form for all transactions. Why does that matter?

Well, recall that the agencies opened about 185 preliminary investigations in FY 2023 out of about 1,805 HSR reportable transactions. The historical rate floats around the same range, i.e. about 10 percent of HSR reportable deals are subject to the costs of responding to a VAL. Why 10 percent? Usually because those are the deals the agency decides have any potential for competitive risks. You can think of the HSR process as one designed to identify the deals that require further analysis by the agency to decide whether to sue or seek relief.

The new HSR form – as you will see – asks for VAL style information for each and every reportable transaction. So using FY 2023 as an example – the 1,620 deals that the FTC concluded required no further analysis because they raised no antitrust issues would now be subjected to something along the lines of an extra 3 weeks and $300,000 to file. A merger tax indeed. The Final Rules applies that tax to every single reportable transaction – including to a large set of transactions that raise no competitive concerns.

The point for now is that Final Rule is very costly. We will get to the question of potentially offsetting benefits shortly.

But however bad the Final Rule is, it could have been much, much worse. Let’s talk for a bit about the Proposed Rule and what we ended up with – with the understanding that the difference is a good measure of the joint marginal product of the two Republican Commissioners Holyoak and Ferguson.

The Proposed Rule Was Wild and Probably Unlawful

Back in June 2023, the FTC published a Notice of Proposed Rulemaking (NPRM) to amend its HSR Rules. That was before the two Republican Commissioners had arrived at the FTC. The new HSR regime contemplated by the NPRM was outlandishly expensive and broad for all transactions. The Proposed Rule would have given the agencies authority to seek information totally irrelevant to the Clayton Act inquiry – recall, the purpose of the HSR Act is to inform Clayton Act analysis of mergers and acquisitions – and introduced a broad tax on all mergers in the form of HSR compliance.

How bad was it? Let’s go through some of the more aggressive proposals. Recall again that this information would be due with the filing of the HSR form for all reportable transactions – not those that are cleared for a preliminary investigation or that the agency has determined raise concerns. Each and every one of them. Here are some examples of new information that would have been due from both merging parties at the time of filing under the Proposed Rule:

Narrative explanations of current and future potential competitive overlaps between the parties supported by sales information, customer information, contracts, and more.

Note that this also will often require some analysis by the filing party about what products are “in” or “out” of a relevant market for antitrust purposes – these responses are not merely clerical in nature

Narrative explanations of any vertical relationships between the parties

Labor market information, e.g.

Providing the aggregate number of employees for each occupational code (SOC)

Identify penalties or adverse findings from various labor authorities (NLRB, OSHA, WHD, etc.)

Identifying overlaps in labor markets

Broadening the scope of Item 4(c) and 4(d) documents to include documents prepared by or for “supervisory deal team leads” in addition to just officers and directors

Drafts (not just final versions) of all final Item 4(c) and 4(d) documents (this is a big one)

Detailed information on all prior acquisitions in the last 10 years

Projected revenue streams for pre-revenue companies

A lot of changes targeting private equity firms and their portfolio companies, e.g.

A description of the filer’s businesses and services

Expanded identification of minority investors

That is just a summary. And as I wrote to start the column, estimates concerning the burden here ranged from 300 hours of attorney work and about $300,000 per firm to file the HSR form.

The big question here from both a legal and economic perspective is whether all that extra cost – applied to every single HSR filing rather than targeted to those transactions that might create competitive concerns – can generate larger benefits?

We will close on that question.

But first, it is worth taking a second to note that the Final Rule included some but not all of those changes above. And that is because the Republican Commissioners were able to bargain out some of them in exchange for a unanimous vote on the Final Rule.

Two Cheers, but Not Three, for the Republican Commissioners

The Republican Commissioners had a tough strategic decision to make. The NPRM version of the HSR Rule was awful and likely unlawful as well. They could either: (1) use their capital to extract as many concessions in the Final Rule as possible and allow for a unanimous 5-0 vote on the item; or (2) allow the NPRM version to pass with a 3-2 vote, and write dissents that pave the way for a legal challenge.

One interesting observation is that Chair Khan apparently cared about this item passing unanimously. I’m not sure we have seen that before. That seems to be a bit of an evolution. And I think that is both worth pointing out as well as giving credit where it is due. But aside from that, a 3-2 vote would have likely subjected the entire economy to a much broader and burdensome rule – so long as it lasted prior to legal challenge. That is a real cost, to be sure. On the other hand, the magnitude of the benefit of the first strategy depends upon exactly what concessions Commissioners Ferguson and Holyoak were able to extract. On that front, they were quite successful.

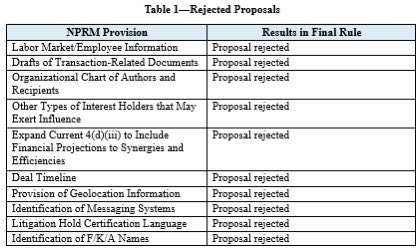

Commissioner Holyoak provides a useful table of some of the spoils of compromise in her dissent:

Labor market specifications? Gone. Some close observers of the FTC might recall the Memorandum of Understanding the FTC signed with the NLRB (which would have allowed them to request some of the same information and share it with the FTC – a cute end around the HSR). That is gone too. Now we know why.

Drafts of transaction-related documents rather than just final versions? Gone. Same with a number of other proposals that were modified rather than eliminated. Commissioner Holyoak has a chart for those too:

The biggest ones here, I think, are preventing the prior acquisition lookback from extending to 10 years (it is 5 years instead), and limiting the request for ordinary course documents to those the CEO has been provided. And perhaps the biggest win was the “return” of the possibility of Early Termination of investigations – a program the Biden FTC ended in February 2021 with a “temporary suspension” due to the pandemic. I am glad to see the ban on Early Termination lifted, though the possibility remains theoretical until we observe the Khan FTC put it to use.

These are some major concessions. And one cheer to the Republican Commissioners for extracting a high price for their vote. If we were grading the execution of the “compromise” strategy in a vacuum – it would be an A+. Some of the worst parts of the Proposed Rule are gone thanks to their efforts. Things could have been much, much worse. I speak from experience in saying I know that it can take significant effort and capital inside the building to battle for these sorts of changes with tangible results. And they did that here.

A second cheer to the Republican Commissioners for unequivocally pointing out in their statements that the NPRM as drafted was not lawful. Both Commissioner Ferguson and Commissioner Holyoak have long and thoughtful statements in defense of their positions. You should read them both.

Commissioner Ferguson persuasively describes, for example, why the NPRM’s Labor Markets instructions violated the Administrative Procedure Act (APA) and were not “necessary and appropriate” to identify transactions that violate the antitrust laws:

Similarly, Ferguson correctly responds to Commissioner Bedoya’s defense of those rules. Bedoya argues that because the antitrust laws can be applied to labor markets the FTC is well within its rights to ask for any and all labor market information in the HSR filing. That, of course, makes no sense.

The APA requires more than that. It does not allow for the imposition of large burdens where there are only small benefits, precisely because the agency could not produce a “rational connection between the facts found and the choices made.” Ferguson emphasizes as much and rightly so:

He points out that in terms of record evidence of antitrust problems arising in labor markets in the Clayton Act context, we do not have enough to believe that expanding the burden will allow significantly greater detection of these problems. We do not have evidence that we are missing a bunch of mergers that would harm labor markets and so the costs of the NPRM would greatly outweigh any benefits and the connection between the NPRM and the HSR Act are tenuous at best.

Ferguson makes a similar point about the NPRM’s requirements regarding deal documents. Again, he is correct. The NPRM would have required production of every single agreement between the parties despite the fact that the rate of return for imposing those costs in terms of enforcement benefits would likely be zero:

Mismatch of costs and benefits indeed.

Commissioner Holyoak raises similar issues concerning the NPRM’s introduction of enormous costs without offsetting benefits. With respect to the NPRM requirement to produce information about workplace safety, she rightly points out it would have “provided no measurable benefit to the agency in its initial determination of whether the proposed merger violates the antitrust laws” and appeals to the lack of empirical evidence available to support the NPRM.

To the extent the FTC attempts to appeal to evidence of rising concentration levels as evidence that it has missed anticompetitive mergers under the old HSR rules, Commissioner Holyoak points out there is no such evidence in the record that would justify the NPRM rules:

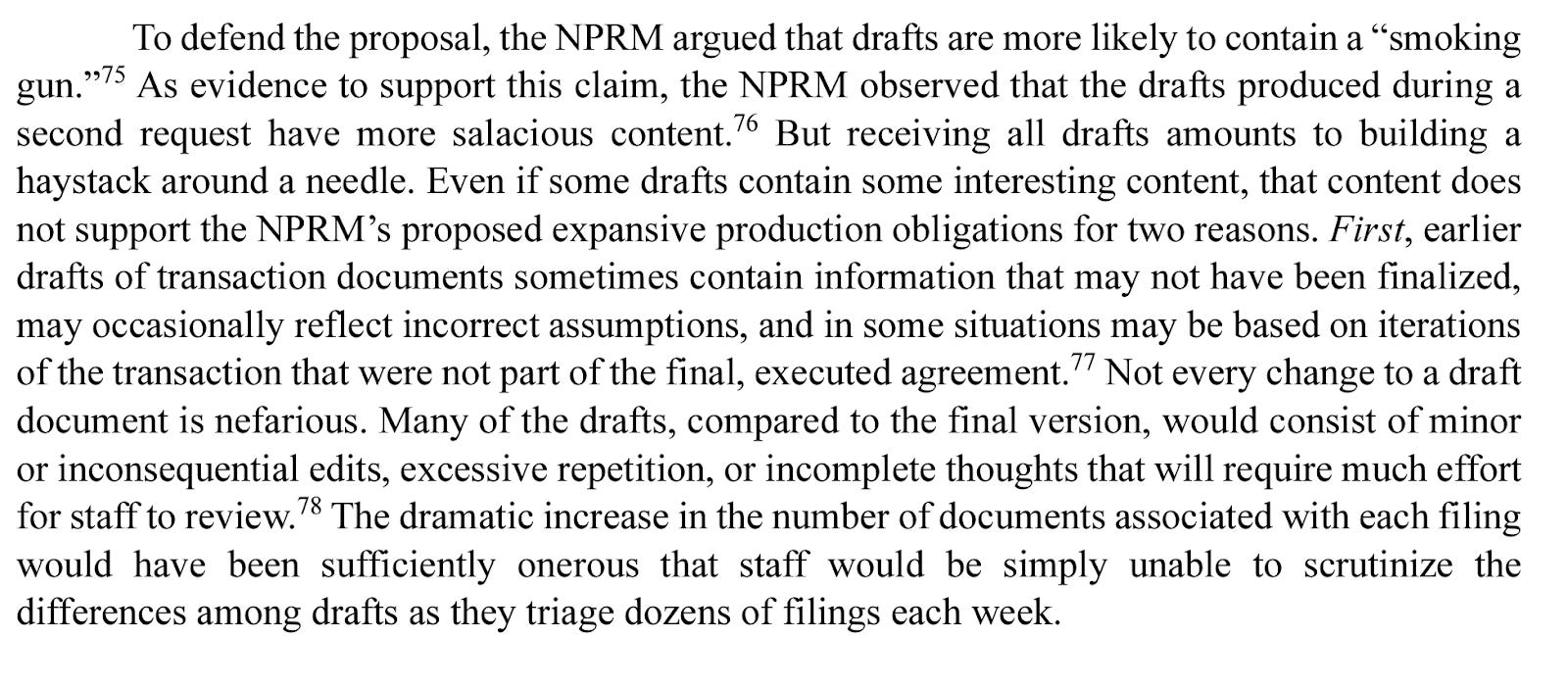

She does the same, again persuasively, to reject the NPRM’s proposal that HSR filers include all drafts of deal documents in the filing:

You get the point. Commissioners Ferguson and Holyoak again and again reject the NPRM proposals because the record evidence that they would generate tangible enforcement benefits that exceed their significant costs is completely absent. And they are right each time.

So why two cheers for Holyoak and Ferguson and not all three?

Because the same exact logic applies to the rest of the changes in the Final Rule.

Both Republican Commissioners offer up a fairly thin argument that the Final Rule would survive judicial review under the APA but the Proposed Rule would not. Commissioner Ferguson makes the most direct case that the vast expansion of required information in the Final Rule is “necessary and appropriate” to the HSR mandate. You should read it in its entirety. I will share here that I do not find it persuasive.

For example, Commissioner Ferguson argues that the Final Rule requires disclosure of investors that own at least 5 percent share in entities related to the acquiring person – including limited partners with management rights. This is, of course, less onerous than the NPRM version which required much broader disclosures. But the only offer of a defense that the expanded rule is “necessary and appropriate” is that there are more transactions today involving funds or limited partnerships than there used to be:

Fair enough. That concern certainly is a theoretical possibility. But do the Agencies have any evidence that the increased social cost of this requirement will generate enforcement benefits beyond identifying a theoretical concern? Evidence of “false negatives,” i.e. anticompetitive transactions the agency missed because it did not impose this burden and have this information at the HSR filing stage? It does not cite any and I’m not aware of any.

When Commissioners Ferguson and Holyoak reject various NPRM proposals they are quick to point out the lack of evidence supporting the proposal, as I pointed out above. The accepted compromises in the Final Rule are plagued by the identical lack of evidence. The point is not to answer whether or not the Republicans got a good deal out of the majority for acquiescing to the Final Rule. A reasonable observer could only conclude the Commissioners were the shrewdest of negotiators.

But from a judicial review perspective it is worth pointing out that the compromise Final Rule simply does not offer up much in the way of supporting evidence to demonstrate the Final Rule will result in any benefits to offset its significant costs.

There are other examples. What of the Final Rule’s significant requirements for disclosing all potential vertical relationships? What evidence that this will improve Clayton Act enforcement by detecting anticompetitive deals that would not otherwise be identified? Some discussion that the agencies have brought more vertical challenges as of late. Of course, they identified those objectionable deals under the old HSR rules. What evidence that the new requirements would help identify otherwise undetected and anticompetitive mergers? Again, a lot of theory but no empirical evidence or even anecdotes about what would change under the Final Rule.

Perhaps the most peculiar feature of the Republican Final Rule compromise is that at least part of it appears based upon the view that the Commission is most likely to use the additional information to be more efficient, more accurately identify transactions with no competitive issues, and avoid preliminary investigations and Second Requests more often. The parties should be grateful to bear these costs, really. OK, they do not quite go that far, but almost. Here’s Commissioner Ferguson:

There are a number of problems with this sort of analysis.

The first is that it identifies the real problem – abuse of merger process by the FTC – and walks right past it. Yes, the FTC is willing to open preliminary investigations but refuse to close them even when there are not competitive issues. But that is misconduct by the agency! And it is misconduct in the merger review process that Commissioner Ferguson and Holyoak have led the way in identifying and fighting! For example, both held the FTC majority to account for their actions in flouting the rule of law and merger process to punish individual oil executives in the Exxon/Pioneer and Chevron/Hess acquisitions.

The analysis defending the Final Rule pretends that this problem would be solved if parties just gave the FTC more information. As if information and evidence, not bad behavior, was the issue for Mr. Sheffield or Mr. Hess. The expanded information requests now due at the time HSR is filed simply give the FTC more levers to pull in the merger review process. And I can assure you that neither merging parties nor third parties believe the supposition that with more information the FTC would simply go away where it finds no competitive problems. Again, this is the FTC that got rid of Early Termination – the mechanism to deal with such mergers and had to be forced – thanks to Ferguson and Holyoak – to bring it back.

The second problem is that, again, there is no evidence to support any of the speculation about greater information resulting in more accurately identifying anticompetitive transactions or reducing the burden in cases where there are no competitive concerns. It is all theory. No evidence. The FTC can and should do better. The problem is that the two Republican Commissioners, at current, are the institution's best hope for holding the FTC accountable when it comes to cost-benefit analysis. To their credit, they have done exactly that in fighting against poorly designed 6b studies and beyond. But that zeal for analytical rigor and evidence appeared to take a back seat here to generate the compromise that is the Final Rule. Again, that might be a good trade? I tend to think not. But your mileage may vary.

Third, a problem that has plagued most of the discussion defending the Final Rule is that it includes a number of broad statements about how gathering more information helps agency decision-making. But all too often the statements do not ask the critical economic question: compared to what? Here the agency can always open a preliminary investigation and get the information it seeks by issuing a VAL or a Second Request. So we really are not talking about whether the FTC has or does not have the relevant information. The Final Rule imposes preliminary investigation burdens on every single HSR filer. So the FTC gets the information more quickly. But in many of these cases it would have access to it one way or another during the HSR process.

For the very large social cost – essentially implementing a broad based tax on all merger activity in the entire economy by requiring preliminary investigation level burdens at the filing stage – one would like to see some evidence that the benefits exceed the expected costs. That evidence is nowhere to be found in the majority or Republican statements.

Does that matter? The Admin Law crowd may be quick to point out that the APA does not require an exacting benefit-cost analysis to justify an HSR Rule change. Indeed. Commissioner Ferguson’s statement gives a masterful discussion of precisely what is and is not required. Of course, the Final Rule cannot be “arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with the law.” Ferguson explains the APA really does not require too much of the FTC:

OK, but can we pause on that bit about “examining the relevant data and articulat[ing] a satisfactory explanation for [our] action including a ‘rational connection between the facts found and the choice made”?

Here, the choice is to impose the social costs of a preliminary investigation – previously reserved for about the 10 percent of filings most likely to cause competition concern – on all acquisitions across the economy. Where is the data supporting that decision? Or the rational explanation? When it came to features of the Proposed Rule like the Labor Markets instruction or the requirement to submit all drafts of transaction-related documents,Commissioners Holyoak and Ferguson were comfortable rejecting the proposals because there was no evidence that enforcement benefits would exceed the costs.

For example, with respect to the Labor Markets instruction, Ferguson argues that the majority’s appeal to “a couple of papers and a book” could not possibly satisfy the requirement that it examine “the relevant data and articulate a satisfactory explanation for [our] action including a ‘rational connection between the facts found and the choice made.”

Well, what is good for the NPRM goose is good for the Final Rule gander when it comes to that standard. And I would contend the Final Rule compromise fails just as plainly. Again, your own mileage may vary. But I do not find the APA defense of the Final Rule persuasive. And I think it is important to point out that while the benefit of the Final Rule compromise might be avoiding a much harsher rule so long as it survives judicial review, a cost not often discussed is the missed opportunity to increase the probability that the Final Rule (or NPRM on a 3-2 vote) fails judicial review.

That decision is a really tough one. The question of whether the Republican Commissioners drove a hard bargain is easy to answer. They sure did. I think most of the bar was surprised to see not only the theoretical return of Early Termination, but also the elimination of the Labor Market and other costly provisions from the NPRM to the Final Rule.

But that is a different question than did the Republican Commissioners make the right choice? The alternative path would have been accepting the NPRM as the “new” HSR rule while writing dissents to pave the way for reversal. I tend to favor the latter path for a number of reasons, including the fact that the latter path, to me, is the one that is more tethered by cost-benefit analysis and economic thinking. But again, reasonable minds can differ on these things. Especially with the Khan FTC, the best hope for institutional defense of economic analysis and the rule of law remains the Republican Commissioners. They have played that role remarkably well in other settings.

Legal challenge to the Final Rule is inevitable either way. A unanimous vote makes a challenge less likely to succeed on the margin. By how much, I do not know. I will reserve commentary on the likelihood that a legal challenge prevails until one is filed.

But the bottom line is that the FTC’s Final Rule is a revolution in the merger review process. Voluntary transactions – all of them, including with no antitrust issues at all – will be up to their neck in the bureaucratic and regulatory costs previously reserved for the most risky 10 percent of transactions. Many will be strangled by these costs in the boardroom or before. But the process pain is the very point of this HSR Final Rule. Again, if your worldview is that mergers are bad then a tax on mergers is a good thing. But make no mistake, this is a large regulatory tax on all mergers. And one that will have a disproportionate effect on smaller firms.

The Final Rule is a monumental imposition of costs across the economy, from small firms to large, manufacturing to retail, oil and gas to private equity. And of course, the Final Rule is a unanimous vote against the Little Tech Agenda. Merger process, not litigated cases, are where the economic action is. And the political action is never too far behind. Watch this space carefully.

But there is another even bigger tax for those deals reviewed by the FTC--resurrection of Part 3 litigation in merger reviews.